When the U.S. central bank raises interest rates and keeps them elevated, investors should position toward must-buy income stocks to buy. Risk-free cash invested in various funds will pay close to the Fed Funds rate. When the next set of economic data confirm that inflation is persistent, yet the job markets are strong, it will keep borrowing costs high.

Investors should accumulate companies that pay a dividend income. That income, plus the upside from these stocks’ potentially rising price, should return more than 5%.

{kind=link}

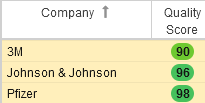

These income champs have great quality scores. (Data courtesy of Stockrover)

In the table above, investors have three high-quality stocks to consider. They are each top options I think are worth buying now.

| MMM | 3M | $107.09 |

| JNJ | Johnson & Johnson | $154.09 |

| PFE | Pfizer | $40.34 |

3M (MMM)

3M (NYSE:MMM) bounced back from a 52-week low, which coincided with Department of Defense data revealing no hearing loss among most plaintiffs suing it for its allegedly faulty earplugs.

More than 175,000 plaintiffs blame 3M’s earplugs for their hearing loss. However, the DoD found that 90% of plaintiffs have no hearing impairment.

MMM stock is a must-buy income stock, for more reasons than just the recently-declared dividend of $1.50 per share. Though, this dividend does represent a 0.7% increase from its $1.49 a share dividend, and marks over 100 years of uninterrupted dividend payments.

3M is navigating through soft demand in the electronics market. Once the de-stocking in technology and industrial products ends, 3M’s business will rebound. The Chinese New Year slowed the industrial end markets in the last quarter. As the market exits that event, demand should improve.

In the U.S. market, the current warm winter will lower energy costs. That should strengthen 3M’s business in the country. In Europe, the year started with solid automotive build rates, meaning there’s plenty of continued momentum for MMM stock right now.

Johnson & Johnson (JNJ)

Johnson & Johnson (NYSE:JNJ) has the vision to develop products to treat multiple myeloma. The company submitted a submission to the U.S. Food and Drug Administration for Darzalex in 2020. This drug is the company’s backbone for myeloma therapy. I think this key drug could provide the company with renewed growth and a more positive outlook from investors.

The company is working toward growing its pharmaceutical group through 2025. Although it will lose the exclusivity of Stelara, J&J will have a $60 billion revenue pipeline by 2025. Thus, this is a company with an impressive portfolio that should drive significant growth. Additionally, the company is working on some potentially blockbuster drugs. Another one I’ve got my eye on is Tremfya, which treats plaque psoriasis and psoriatic arthritis.

When J&J presents its data readouts for its inflammatory bowel disease in ulcerative colitis and Crohn’s disease this year, investors will likely be quick to update their growth outlooks for both Tremfya and the entire company. Spravato, which treats schizophrenia and bipolar disorder, is another growth catalyst to consider.

J&J’s Carvykti drug helps the patient’s immune system fight multiple myeloma. This product is among the many growth catalysts I think the market is overlooking right now.

Pfizer (PFE)

Pfizer (NYSE:PFE) peaked at almost $55 late last year before falling to around $40. That said, like J&J, Pfizer is a company with plenty of innovation that should drive its long-term growth.

Pfizer aims to add $25 billion in risk-adjusted revenue by 2030 from external innovation. The company plans to accomplish this by pursuing meaningful acquisitions to accelerate the development of its pipeline. In other words, the drug company wants to add to its core therapeutic areas.

Pfizer improved its R&D productivity in the last several years, leading to increased demand for its R&D resources. To maximize returns from those efforts, it prioritized its pipeline. It allocated its energy to promising medicines. Thus far, this strategic review hasn’t impacted its stock price. However, over the long-term, I think Pfizer is an undervalued Pharma stock worth buying.

On the date of publication, Chris Lau did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.